5 Financial Mistakes to Avoid

Blog

Although there are no strict rules when it comes to handling your finances, there are a number of common financial mistakes that I often see with clients. Many of these can be avoided and it’s largely about approaching your money from an expansive, empowered place in addition to bringing financial education into the equation.

Here are my tips on 5 financial mistakes to avoid.

Paying someone else interest with your money

This is one of my key pieces of advice when it comes to creating wealth. If you’re relying on debt instruments, you’re essentially paying someone else interest with your hard-earned money! Imagine what you could do with those funds and how you could instead, allocate them towards your financial future. Set the goal to pay off any debts and avoid restarting the cycle. For example, if you complete your car payment and want to purchase another car, have your own funds in place to do that without using further lines of credit.

Becoming your own bank is a gradual process but once you set that intention, it creates energetic financial expansion and becomes incredibly empowering to know you’re on your way to true financial independence, freedom and flexibility!

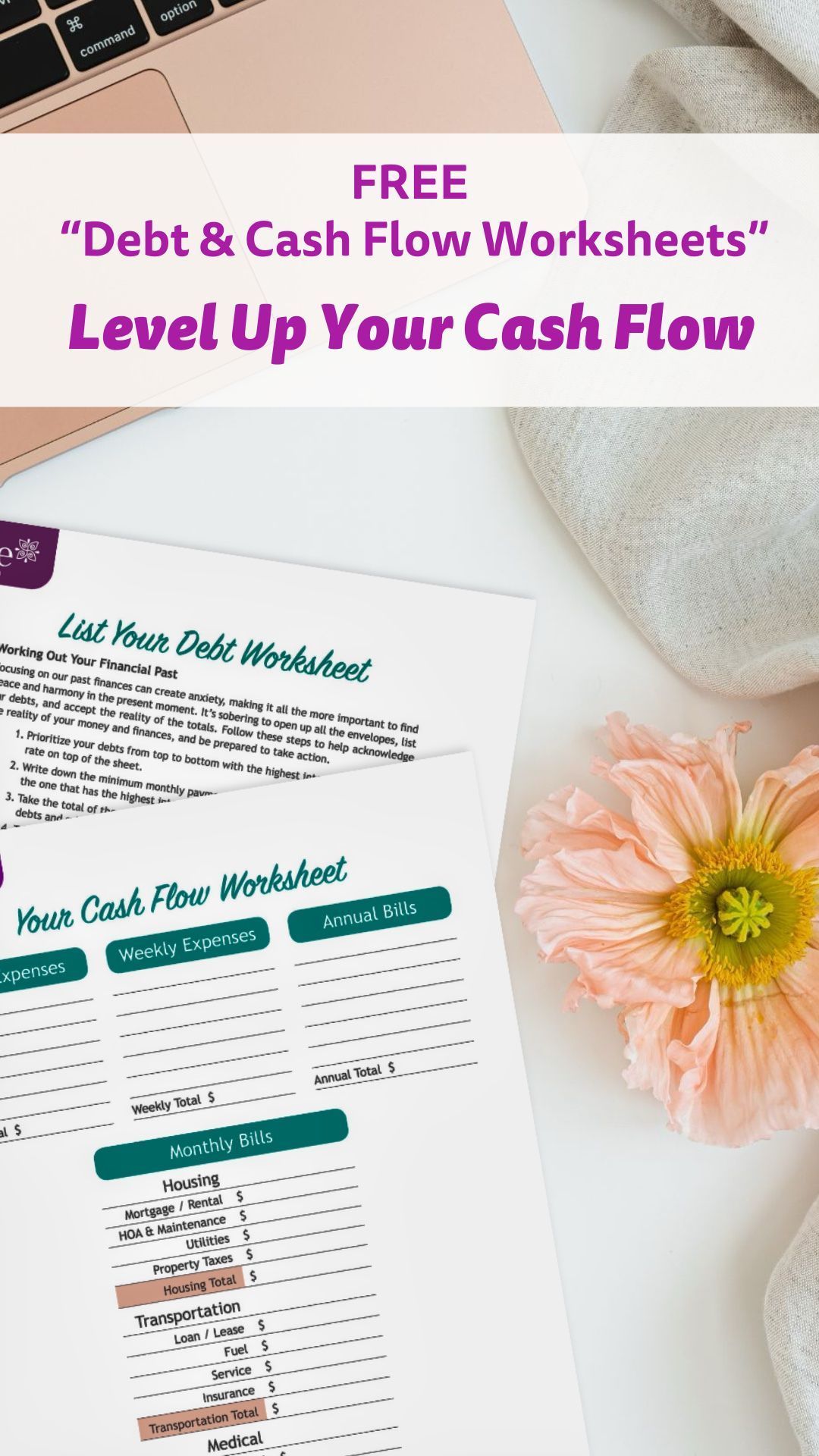

Not having an emergency reserve fund and turning to credit lines

This is one of those financial mistakes that is often overlooked but is incredibly important. We never know what emergencies and situations can come up and when we don’t have any money specifically set aside to take care of them, this is when we panic and rely on credit lines. Consequently, we’re then paying for the emergency long after it’s taken place.

My suggestion is to start a dedicated online emergency reserve account where every month, a portion of your income is deposited. This way, you’ll be building up funds to take care of any unexpected emergency costs and it will remove any stress and anxiety about how those costs are going to be handled. Again, this is all about becoming entirely self-sufficient with your money and not having to rely on anyone else to take care of your needs.

Create a House Maintenance fund

How often have you needed to replace something in your home and then had to allocate a substantial portion of your money that was intended to be spent on something far more fun or pleasurable towards it? Let’s face it, house maintenance costs can be expensive but by putting a financial intention in place for them, there’s no reason why they have to be stressful.

I suggest you put $250 per month into a House Maintenance savings account and over 20 years you’ll be able to pay cash for those new windows, a replacement roof, new appliances, a dishwasher, washing machine or air conditioner. All of these big-ticket items can throw your personal cash flow through a loop, but by having the money there in place already and ready to go, they can get taken care of without having any impact on the rest of your finances.

Stop financially bailing other people out

Are you that person who always seems to be rescuing others financially? Perhaps it’s your children or family members and somehow, you have become their go-to when in a financial fix? Or maybe you’re always insisting that you help them out?

This is about creating both financial and personal boundaries. If you’re always there to bail your child out for example, they’ll come to expect it and won’t have any reason to gain their own financial education to make different choices. I talk a lot about creating more empowerment with our money but the same goes towards offering this to other people. The greatest act of love you could give your child - or anyone relying on you financially, is to step back, give them the space for their own expansion to occur and to build their own financial muscles. Of course, it doesn’t mean you have to abandon them and you can still be there to support them emotionally. But what they will gain from creating their

own financial independence is truly priceless and they will be grateful to you in the long-term.

Don’t create financial leaky containers

A big financial mistake I see is the creation of leaky financial containers. An example of this could be someone working so hard to earn as much money as possible, but as a result they’re ignoring their relationships or health. Over time, the impact of this compounds leading to relationship breakdowns, divorce and unexpected health costs. All of these eventually come with financial consequences later in life - and typically very costly ones! These are what I call leaky financial containers.

Creating what I call Real Wealth is about looking at your life through its full lens. Nurturing your relationships, taking care of your health and doing work that lights you up.

A further example is paying interest to a bank. You are not in a place of empowerment if you’re carrying credit card balances month after month. The leaky container is the interest that you’re paying, which let’s face it; none of us feel good about! This is again going back to the idea of becoming your

own bank and setting healthy boundaries for yourself.

I talk a lot about this on my

YouTube channel and I’ll be expanding much more on this idea of leaky financial containers in a future article, as they’re one of the most common financial mistakes I see in my work.

Wherever you’re starting from, by putting the above tips in place, you’ll already be on your way to avoiding most of the financial mistakes I often see. This is about creating alignment, expansion and

true financial independence.

Share Blog On Social

Recent Blogs

Similar Blogs