Money/Cash Flow

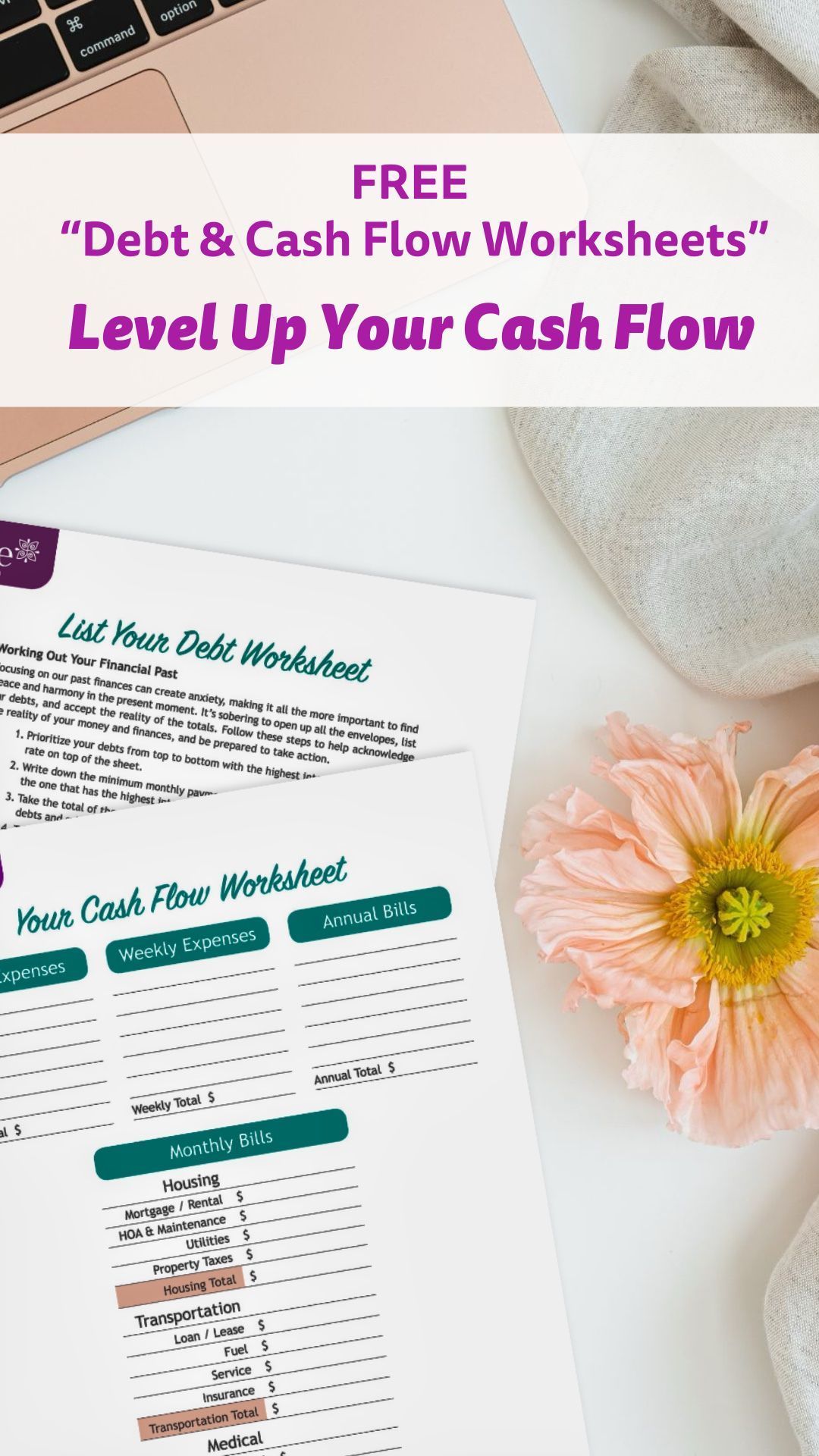

Think back to a time when you earned very little income. Remember how it seemed like you pinched every penny, but there still wasn’t ever enough? I’m going to bet that you probably feel pretty close to that today, despite the fact that you make much more money. It has become second nature to increase our standard of living in proportion to our income. The biggest challenge I see here is that if you continually increase your spending, and you don’t increase your savings level, at some point in your life you’ll have to decrease your lifestyle. You’ll have to live in retirement at a lower level of income than you were in the decade before you left the workforce.

Many people have said to me that once they retire, their house will be paid off, the kids will be on their own, and they won’t need as much money in retirement. The reality I’ve experienced is that, yes, most people do have more disposable income after they pay off their homes and their children grow up and leave. What many clients fail to realize, however, is that they are still going to need a substantial income, because they want to travel more, spend more on grandkids, etc. And that doesn’t even factor in inflation. Plus, if you’re not working, what will you do to fill your time? In most cases, retired people don’t spend less money; they just shift what they’re spending their money on. That being said, there are plenty of ways to create some wiggle room with your cash flow. We’ll get to that shortly.

The post Money/Cash Flow appeared first on Julie Murphy.

Share Blog On Social

Recent Blogs

Similar Blogs