Don’t Be a Slave to Debt

Have you ever noticed how advertisements for credit cards are always so positive? They talk about their zero interest rate and high lines of credit. They entice you with colorful type, glossy paper and a pre-printed plastic card with “preferred customer” displayed in place of a name. And they always talk about how manageable their balance will be. No need to be concerned about your bill getting out of hand; this credit card is better than the others. Less hassle! Better interest rates! A company that cares!

Have you ever noticed how advertisements for credit cards are always so positive? They talk about their zero interest rate and high lines of credit. They entice you with colorful type, glossy paper and a pre-printed plastic card with “preferred customer” displayed in place of a name. And they always talk about how manageable their balance will be. No need to be concerned about your bill getting out of hand; this credit card is better than the others. Less hassle! Better interest rates! A company that cares!

How often have you fallen for that scheme? The pretty paper and encouraging words can be quite the draw, especially when you are in need of some extra cash to help keep your kid in college or to assist in caring for your ailing parent. So you sign up, promising yourself that this time it’ll be different. You’ll pay off the balance at the end of the month. You’ll only use it when you absolutely need it. And you won’t overspend just because you haven’t reached your max yet.

Six months and thousands of dollars later, you find yourself with another five-figure credit card bill and a pit at the bottom of your stomach. How did I end up here again , you ask yourself. Why did I do this? I know better.

Well, I’m here to tell you to things. The first is that you are not alone. Forty-three percent of Americans spend more than they earn each year and 46% of all Americans carry a credit card balance from month to month. All of us, at one time or another, have found ourselves in a financial quandary in our lives. Either we’re in over our heads because of student loans; house poor because of a mortgage we can no longer afford; or we sank into the credit card trap. Not only is this is no reason to feel shame or guilt, it is a fixable problem.

But the other more important lesson I want you to take away from this is that nothing is more valuable than your instincts. As good as that new credit card with zero interest for the first year may sound, you know in your gut what it can lead to. What it will most likely lead to.

Action step

Being a slave to your debt means staying on the merry-go-round of the debt cycle. Never paying it off and carrying over balances month after month. Continuing to max out credit cards or using one credit card to pay off another. Buying a car or signing for a mortgage that you can’t afford. It means not changing a thing about the current state of your finances and still hoping they will magically change themselves.

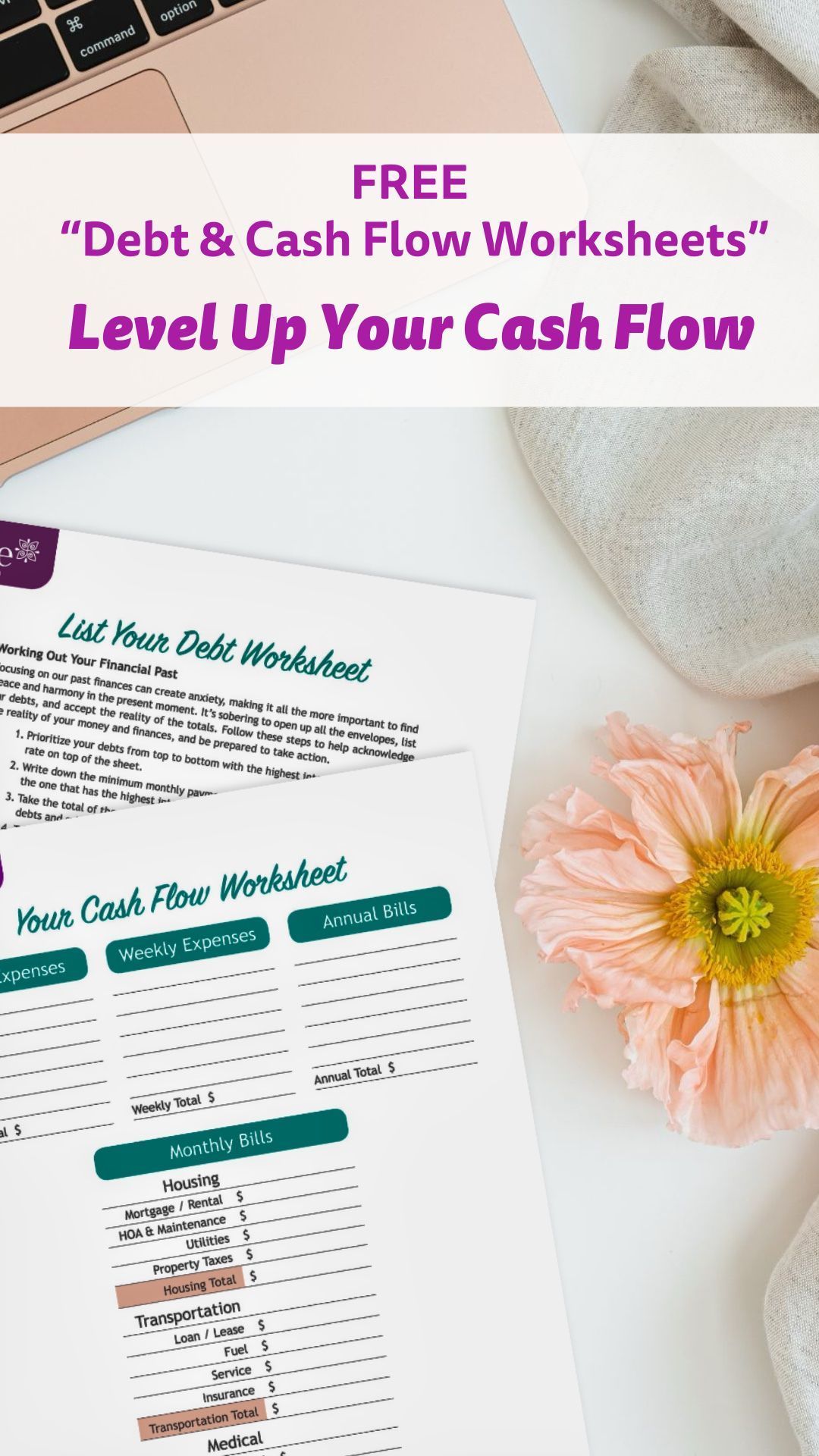

I’m here to tell you that you can absolutely break free of the cycle. You can regain control of your finances – today, right now – by first making the choice to do so. Start small. Take your credit card with the least amount due and carve out a plan to pay it off. It may take a few sacrifices, but it will be worth it in the end. Figure out the things that aren’t all that important to you and devote that money to taking charge of your debt.

Relentlessly cut back on the things that you don’t want or like or need to have and use your whatever is left (after putting some on the credit card) to do something that is right for you. Funnel it into your dream of starting a business or taking a Hawaiian vacation. Invest or save it. Or buy that pair of shoes you’ve been eying for months now. Whatever you choose, celebrate it. Know that you are both fixing your past and living in the right now all because you made the decision to take back control over your debt.

Like this blog? Share it with your friends on Facebook and Twitter. Also, be sure to sign up for my bi-weekly newsletter Financial Consciousness. And join the conversation on Facebook where we’ve grown together and act as a community to promote financial healing.

The post Don’t Be a Slave to Debt appeared first on Julie Murphy.

Share Blog On Social

Recent Blogs

Similar Blogs